[Fifth in a series. The beginning is here]

You need to get the numbers right

Earlier, we said that “fiat money,” namely the US dollar, is backed by NOTHING. True in the physical sense, as there are no precious metals waiting for you to pick up at Ft. Knox in exchange for your Federal Reserve Notes (FRN).

However, hope springs eternal... One might argue that, psychologically, FRNs are backed by confidence in the US Government. Back in 1957, in a country being run by The Greatest Generation that had just won a World War, “the full faith and credit of The United States of America” had meaning. Today, with the youngest generation in the basement counting body piercings paid for by their parents, not so much.

Remember that 5-pound bag of charcoal that sold for $5 in my class 16 years ago? Today it sells for $10. If, rather than buying charcoal then, you put your $5 in a bank that returned 4.43% per year for 16 years you would have “broken even” because you would have ten Federal Reserve Notes today to buy charcoal. But during that particular time, banks paid nearly zero on deposits. Thus, by inflating the money supply for 16 years your purchasing power eroded by half. There is your inflation tax.

Your government even admits this, but you must look hard to find it. At this link, the Bureau of Labor Statistics (BLS) will compute inflation for you. Put $5 in the first field, August, 2008 in the second and July 2024 (16 years later) in the third field and you get a dollar answer, $7.18. Back to the bank. Putting $5 in at 2.29% interest produces $7.18 after 16 years.

Hold it!! A moment ago, we said it was 4.43% per year inflation, now it is 2.29% per year. What gives? You thought the government was going to give you the TRUTH? Silly you. The government has been messing with the inflation calculation for 40 years, always – of course – to force the number as low as possible.

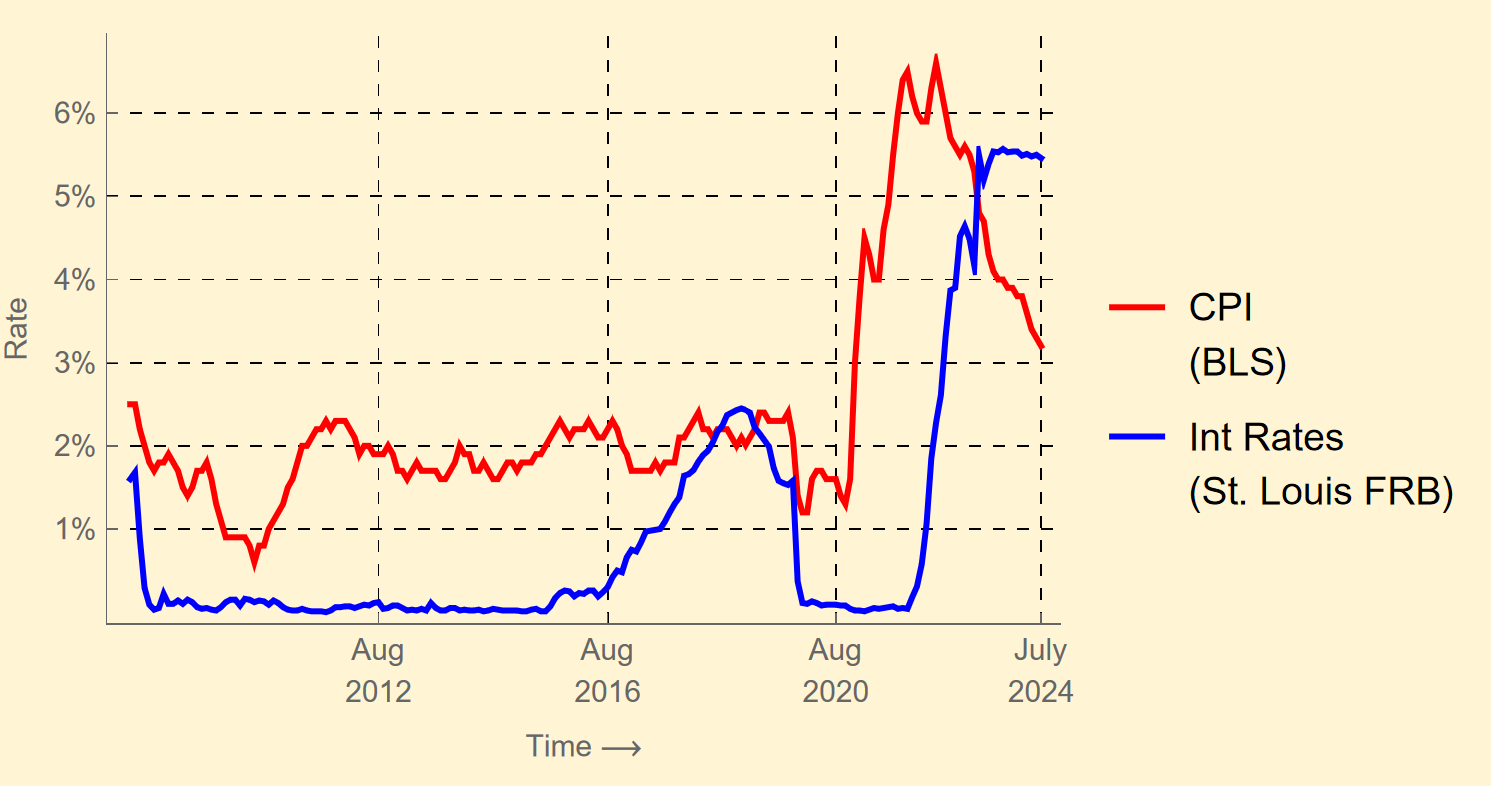

Timing is everything

Below is your life over the past 16 years. The red line is the Consumer Price Index (at least what the government reports it to be); the blue line is the interest rate series over the same period.

Note Well: First, for a decade interest rates were always less than inflation and only more twice, briefly. Second, the lines meet (making inflation the same as interest rates) only three times in 16 years. Third, in order for you to stay even you had to earn as much money on your saved dollar as that same dollar was being devalued. How easy was that? Not very.

BUT, you say, “I can earn a lot more than interest in banks. I can invest in lychee nut plantations in Brazil and make loads of money.” You have now just been manipulated into risk mismatching, something your government wants you to do. This, the most insidious aspect of inflation, changes your behavior. People who were once rational savers who made careful calculations before acting, are now – to ward off inflation – buying dumb things and becoming more like their government.

Many ways to get many answers

There is considerable mythology surrounding inflation. It is much studied and reported on. Theories abound. There are multiple ways to compute it. Arguments can be made that the price on some products (charcoal?) rises faster than the price on others. BLS statistics reflect a so-called “market basket” of products. For the cost of that basket to be the same with charcoal in it at a price rising over time, prices of other things (tires, diapers, steel girders…) must fall. Sound plausible? What have you seen go DOWN in price?

Below we see that the value of money is the inverse of the price level. Assuming no change in production (real wealth), the value of money drops (black arrow) as prices rise. This occurs with the increase (red arrow) of the money supply from M0 to M1.

I have spoken often about the evil and futility of passing laws to make people do things they do not want to do. The pernicious genius of inflation is that you don’t have to pass laws to manipulate people, you just print money in strategic amounts at strategic times.

This is commonly known as “being played.”

[Next week: Time for some technical details]

Roger, I think it helps to show graphs of real, inflation-adjusted rates. I’ve always used the perpetual bond or consol rate of 3 percent per annum to estimate real yields on our investment portfolio.